經(jīng)管學(xué)院教授論文高居金融學(xué)頂刊JFE中國(guó)經(jīng)濟(jì)題材引用量前十

研究中國(guó)經(jīng)濟(jì),講好中國(guó)故事,不僅僅是中國(guó)學(xué)者的重要工作,也越來(lái)越受到全球經(jīng)濟(jì)學(xué)家的重視。香港中文大學(xué)(深圳)經(jīng)管學(xué)院張?zhí)镉嘟淌凇⑼粲孪榻淌趨⑴c的三篇論文高居金融學(xué)頂刊Journal of Financial Economics中國(guó)經(jīng)濟(jì)題材引用量前十,其中張?zhí)镉嘟淌诘囊黄撐囊昧窟_(dá)2741。

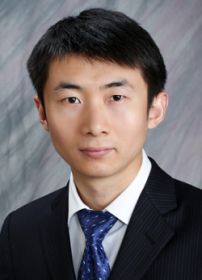

張?zhí)镉?/p>

校長(zhǎng)講座教授

深圳高等金融研究院制度與資本市場(chǎng)研究中心主任

會(huì)計(jì)理學(xué)碩士項(xiàng)目主任

研究領(lǐng)域:

實(shí)證公司財(cái)務(wù)、政治經(jīng)濟(jì)學(xué)、

行為經(jīng)濟(jì)學(xué)、組織經(jīng)濟(jì)學(xué)、中國(guó)經(jīng)濟(jì)

汪勇祥

校長(zhǎng)講座教授

研究領(lǐng)域:

機(jī)構(gòu)與中國(guó)資本市場(chǎng)、

公司治理、媒體和社交媒體

?

期刊介紹?Journal of Financial Economics

Journal of Financial Economics是由Elsevier出版的金融領(lǐng)域同行評(píng)判的學(xué)術(shù)期刊,被認(rèn)為是一流的金融雜志之一。Journal of Financial Economics是三大金融學(xué)頂刊中發(fā)表中國(guó)題材論文最多的期刊,引用量也最為可觀。根據(jù)谷歌學(xué)術(shù)數(shù)據(jù)統(tǒng)計(jì),引用量過(guò)千的論文有五篇。

?

引用量前十

01. Law, finance, and economic growth in China

中國(guó)的法律、金融與經(jīng)濟(jì)增長(zhǎng)

02. Politically connected CEOs, corporate governance, and Post-IPO performance of China's newly partially privatized firms

CEO政治關(guān)聯(lián)、公司治理與中國(guó)混改企業(yè)IPO后的業(yè)績(jī)表現(xiàn)

03. China share issue privatization: the extent of its success

中國(guó)混合所有制改革的成效

04. Tunneling through intercorporate loans: The China experience

通過(guò)公司間借款進(jìn)行利益輸送:來(lái)自中國(guó)的經(jīng)驗(yàn)證據(jù)

05. Institutions, ownership, and finance: the determinants of profit reinvestment among Chinese firms

機(jī)構(gòu)、所有權(quán)和融資:中國(guó)公司利潤(rùn)再投資的決定因素

06. Ownership concentration, foreign shareholding, audit quality, and stock price synchronicity: Evidence from China

股權(quán)集中度、外資持股、審計(jì)質(zhì)量與股價(jià)同步性:來(lái)自中國(guó)的證據(jù)

07. China’s secondary privatization: Perspectives from the Split-Share Structure Reform

中國(guó)的二次國(guó)企改制:基于股權(quán)分置改革的視角

08. Politicians and the IPO decision: The impact of impending political promotions on IPO activity in China

官員與IPO決策:即將到來(lái)的政治晉升對(duì)IPO活動(dòng)的影響

09. Profiting from government stakes in a command economy: Evidence from Chinese asset sales

計(jì)劃經(jīng)濟(jì)下政府持股的益處:來(lái)自中國(guó)國(guó)有股份出售的證據(jù)

10. Size and value in China

中國(guó)的規(guī)模因子和價(jià)值因子

?

經(jīng)管學(xué)院教授論文簡(jiǎn)介

● Politically connected CEOs, corporate governance, and Post-IPO performance of China's newly partially privatized firms

? ?CEO政治關(guān)聯(lián)、公司治理與中國(guó)混改企業(yè)IPO后的業(yè)績(jī)表現(xiàn)

● 作者:范博宏 ?香港中文大學(xué);T.J. Wong ?南加州大學(xué)馬歇爾商學(xué)院;張?zhí)镉??香港中文大學(xué)(深圳)

●Abstract: Almost 27% of the CEOs in a sample of 790 newly partially privatized firms in China are former or current government bureaucrats. Firms with politically connected CEOs underperform those without politically connected CEOs by almost 18% based on three-year post-IPO stock returns and have poorer three-year post-IPO earnings growth, sales growth, and change in returns on sales. The negative effect of the CEO's political ties also shows up in the first-day stock return. Finally, firms led by politically connected CEOs are more likely to appoint other bureaucrats to the board of directors rather than directors with relevant professional backgrounds.

?

● Politicians and the IPO decision: The impact of impending political promotions on IPO activity in China

● 官員與IPO決策:即將到來(lái)的政治晉升對(duì)IPO活動(dòng)的影響

● 作者:Joseph D. Piotroski ?斯坦福大學(xué)工商管理研究生院;張?zhí)镉??香港中文大學(xué)(深圳)

● Abstract:This paper shows that incentives created by the impending turnover of local politicians can accelerate the pace of initial public offering (IPO) activity in certain politicized environments. Focusing on China, we exploit a research setting where politicians are rewarded for capital market development, firms rely on political connections for access to capital, rent-seeking behavior is rampant, and the objectives of the state might not be to maximize capital market efficiency. We find that the rate of exchange eligible firms engaging in an IPO temporarily increases in advance of impending political promotion events. This effect holds for both state-owned and non-state-owned entities. For state-owned firms, the effect is strongest in those provinces where the politicians are more likely to be rewarded for market development activity. For non-state-owned firms, the temporary increase in IPO activity appears to be (rationally) opportunistic in nature, with the effect stronger around events more likely to disrupt the firms' political connections. Promotion period IPOs underperform non-promotion period IPOs in terms of both future financial performance and long-run stock returns, have controlling shareholders who retain a larger fraction of the company, and are more likely to divert proceeds away from their intended use after the offering.

?

● Profiting from government stakes in a command economy: Evidence from Chinese asset sales

● 計(jì)劃經(jīng)濟(jì)下政府持股的益處:來(lái)自中國(guó)國(guó)有股份出售的證據(jù)

● 作者:Charles W. Calomiris ?哥倫比亞大學(xué)商學(xué)院;Raymond Fisman ?波士頓大學(xué);汪勇祥 ?香港中文大學(xué)(深圳)

● Abstract:We examine the market response to an unexpected announcement of the sale of government-owned shares in China. In contrast to earlier work, we find a negative effect of government ownership on returns at the announcement date and a symmetric positive effect from the policy's cancellation. We suggest that this results from the absence of a Chinese political transition to accompany economic reforms, so that the benefits of political ties outweigh the efficiency costs of government shareholdings. Companies managed by former government officials have positive abnormal returns, suggesting that personal ties can substitute for government ownership as a source of connections.

?

文章轉(zhuǎn)自經(jīng)管學(xué)院微信公眾平臺(tái),鏈接為https://mp.weixin.qq.com/s/5DcW9895dzuAvjyCHWBhqw